🚨 BITCOIN MAY STILL HAVE ONE MORE BRUTAL LEG DOWN.

Every major correction lasted around 396 days, and BTC is still inside that same window.

Monthly RSI is also sitting near the same level seen before previous cycle bottoms.

The reversal may come later.

But first, Bitcoin could still flush much lower.

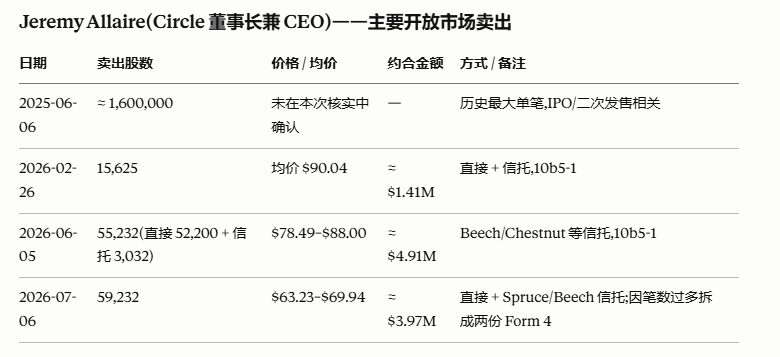

CEO在60多的价格还在卖Circle是我没有预料到的

买入0 笔。第三方数据确认:自 2021 年以来,Allaire 在 CRCL 的全部内部人申报中买入为零;而且整个公司层面所有内部人自 2021 年以来累计买入 0 股、卖出约 1,270 万股——即没有任何一位高管有过增持。 https://t.co/4cxmbYk13V

随着Noxa的关闭,RH链的热点目前主要围绕着应用币展开,一类是以RWA/AI为题材的,例如$INDEX,$STONKBROKER,一类是以发射台为题材的,例如$PONS。

之前介绍过的 @ArrowFinanceio 也即将推出自己的发射台ArrowPad,暂定的上线时间是美东的周一,从团队发布的文章来看,它们更倾向于吸引到高质量的项目和开发者。

另外,Arrow CDP的测试阶段Alpha 0.1也已经在16号上线,并在24小时内达到了配额上限,后续随着智能合约审计完成,会逐步提高上限,并扩大支持的抵押品范围。

RH链的发射台之争还是比较激烈的,看看Arrow能不能在其中占据一个生态位,并配合后续开发的其他DeFi产品套件,构建出一个完整的链上金融生态。

最近美股大幅回撤,比特币竟然纹丝不动?

币圈真的到底了吗,去年 $110000 做空的Doctor Profit,最近全面平空,并转向做多

他自称发布了"世纪报告”,先介绍博士 @DrProfitCrypto 是谁🧵

2026年6月他公开的月度交易总览显示总净收益+800.9%,其中做空部分净收益+760%。做空100多个山寨币时,83个盈利、13个亏损、4个爆仓,一举成名

📌时间回到去年高点

2025年9月,比特币在115k–125k区间高位震荡时,他开始系统性卖出现货并建立空头

每天BTC在这个区间内,就卖掉10%的现货仓位,同时加空头。不管当天是116k还是124k,纪律执行,不犹豫。之后BTC一路跌到60k附近,跌幅超过50%

同时他从2026年4月起做空了100多个山寨币,每个仓位独立$10k、1倍杠杆、孤立保证金,总敞口约100万美元

过去9个月整个加密市场的下跌周期,他几乎完整地吃到了

世纪报告说了什么?

7月18日,他发布了这篇自称世纪报告的长文,核心两个动作,1⃣️全面平掉所有加密空头,2⃣️同时在64,000美元买入比特币现货

买入策略延续了他一贯的机械纪律:

只要BTC在54k–64k区间内,每天投入总分配资金的5%买入现货,上限20天。跌到54k附近会更激进。和顶部卖出时每天10%的节奏完全对称,只是这次放慢到5%,想把积累期拉得更长

📌他的看多逻辑

第一层:情绪面完全反转了

去年BTC在120k的时候,所有人喊15万。现在整个推特都在等4万、4.5万、甚至3.8万。

他说:"当所有人都在等同一个价格时,市场几乎不会给你。"

还有他自己之前也喊过40k–50k是深度熊市目标。但现在这个叙事已经被全网复制了

六个月前没人看这么低,今天每个账号都在喊。他认为当一个目标变成共识的时候,它反而最不可能实现

所以他选择在64k就开始买,宁愿抢在羊群前面,也不跟所有人一起排队等40k🤣

第二层:不信四年周期底部会准时来

现在问任何人打算什么时候抄底,答案几乎都是9月或10月,理由是四年周期

当所有人都根据同一个日历来安排操作时,市场凭什么按剧本走?万一周期不是整整四年,而是三年零九个月呢?底部很可能比散户预期的来得更早

第三层:结构性环境正在发生质变

他认为现在的比特币市场和六个月前已经不是同一个市场了

BlackRock、Vanguard、JPMorgan、Goldman Sachs和纽交所已经在参与DTCC的实时代币化试点项目。微软股票、SPY、QQQ和美国国债正在作为代币化证券进行测试,官方计划10月上线。Citadel刚以200亿美元估值向https://t.co/13svC5LdQG投了4亿美元。CLARITY Act可能在8月10日通过参议院

他的判断是:最大的资本已经在动了,监管框架正在加速落地,而散户还在争论熊市是否结束。他选择跟着大资金动,而不是等散户的确认信

最后

虽然加密仓位全面转多,但他保留了所有标普500的空头

逻辑是加密从125k跌到60k已经完成了重新定价,而美股在同一时间段还在创新高,估值依然偏高

他甚至认为如果美股崩盘,反而利好加密。资金会从高估资产流向低估资产,特别是在代币化和稳定币叙事正热的背景下

这和最近市场的实际表现似乎也有所印证,美股近期大幅回撤,而 bitcoin:native 基本纹丝不动,两者的走势正在脱钩

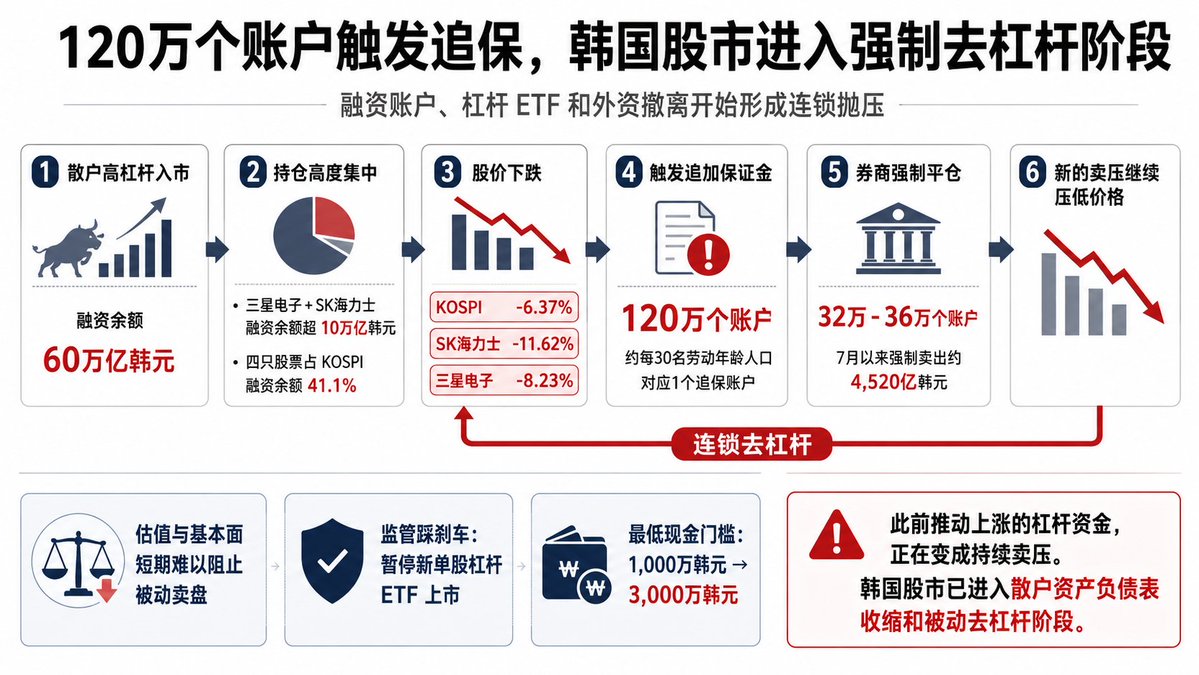

120万个账户触发追保,韩国股市已经进入强制去杠杆阶段

前面我讲过,韩国股市这轮下跌最大的麻烦,是融资账户、杠杆 ETF 和外资撤离同时出现。现在散户融资账户开始被券商强制卖出就意味着高杠杆带来的负面影响已经在开始爆发了。

截至 7月13日,韩国市场已经有超过 120 万个散户杠杆账户触发追加保证金,其中大约 32 万至 36 万个账户已经被券商强制平仓。按账户数量和韩国劳动年龄人口粗略对照,相当于每 30 人就有一个账户卷入追保。

韩国散户借钱入市的规模,在 5 月底已经达到创纪录的 60 万亿韩元。资金又高度集中在三星电子和 SK 海力士,仅这两只股票的融资余额就超过 10 万亿韩元,加上三星电子优先股和 SK Square,四只股票占 KOSPI 融资余额的 41.1%。

这意味着海力士和三星一旦同时下跌,影响会迅速从股价传导到整个融资体系。股价下跌导致账户抵押品缩水,券商要求补充保证金,无法补足的账户被强制卖出,新的卖盘继续压低股价,随后触发下一批追保。

7 月16日,KOSPI 再次下跌 6.37%,SK 海力士下跌 11.62%,三星电子下跌 8.23%。7 月以来,因为未能及时补足资金而产生的强制卖出已经达到约 4,520 亿韩元,日均超过 500 亿韩元,接近上半年日均水平的两倍。

到了这个阶段,公司估值和长期基本面短期内已经很难阻止卖盘。券商处理融资违约时不会考虑海力士是不是 AI 和 HBM 的长期受益者,只会卖出账户中还有流动性的资产,用来填补保证金缺口。

韩国监管部门现在已经暂停新的单股杠杆 ETF 上市,并把投资这类产品所需的最低现金余额从 1,000 万韩元提高到 3,000 万韩元。但监管开始踩刹车的时候,杠杆早已进入市场,政策本身甚至可能刺激部分投资者提前退出,继续增加短期波动。

此前推动韩国股市上涨的杠杆资金,现在已经变成持续卖压。韩国股市也从高波动行情,正式进入散户资产负债表收缩和被动去杠杆阶段。

这也是为什么我会选择做空 SK 海力士的主要原因,因为这就像是 DeFi 的连环暴雷一样,越是下跌越会让更多的杠杆资金爆掉,然后退进价格的下跌。

@Gate Crypto、美股、港股、韩股、黄金、CFD、预测市场一站交易

美国参议院通过两党决议,反对赦免 SBF

美国参议院于7月15日通过 S.Res.772 决议,明确表示无论任何情况下,FTX 创始人 Sam Bankman-Fried 都不应获得总统赦免、减刑或其他形式的联邦宽赦。

决议由民主党参议员 Ruben Gallego 和共和党参议员 Cynthia Lummis 共同提出,并通过一致同意程序获批,没有参议员提出反对。决议还提到,正在服刑25年的 SBF 已于2026年正式提交总统赦免申请。

不过,这是一份表达参议院立场的非约束性决议,无法限制特朗普行使总统赦免权,也不代表参议院进行了100票对0票的记名表决。

@Gate Crypto、美股、港股、韩股、黄金、CFD、预测市场一站交易

MESSAGE To all U.S. Senators: 🇺🇸 America is falling behind.

Pass the CLARITY Act.

🇯🇵 Japan approved landmark crypto legislation.

🇰🇷 South Korea declared crypto a national asset.

🇭🇰 Hong Kong launched regulated stablecoins.

🇸🇬 Singapore keeps expanding crypto licenses.

🇦🇪 UAE is becoming a global crypto hub.

🇪🇺 Europe implemented MiCA.

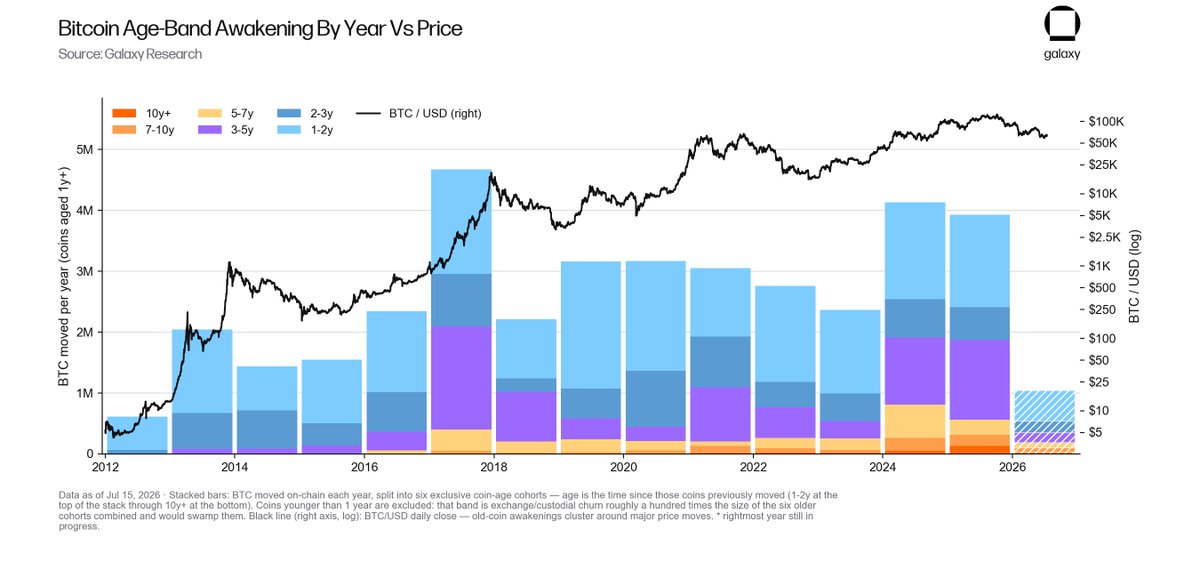

an enormous amount of old BTC came online and moved onchain in 2024 and 2025, rivaled only by 2017

this ‘great distribution’ is mostly over and 2026 is on pace to see less than half the amount of awakened coins as last year https://t.co/QAyjjNACUD

Chinese chip manufacturer CXMT has launched on Hyperliquid pre-IPO perps as is trading 6.25x+ from the IPO price of $1.28 per share.

Insane.

Chinese investors who get access to this IPO will do extremely well. Its up 32% from launch price on Hyperliquid. https://t.co/fe2XFrppV0

BREAKING: South Korea just made crypto part of its national assets.

The new National Asset Basic Act brings virtual assets and intellectual property under state asset law for the first time.

The framework had stayed unchanged since 1950, previously covering mostly real estate.

This comes alongside continued work on the Digital Asset Basic Act, stablecoin rules, and a spot crypto ETF framework.

🔍 One weekly candle doesn't change the trend but where it closes can change the entire narrative.

Compared to my last $ETH update, the reaction from the long-term ascending trendline is the biggest development on the chart. Buyers stepped in exactly where higher-timeframe support was expected, preventing a deeper breakdown and keeping the broader structure alive. 📈

The technical picture is improving, but it still needs confirmation. Momentum is recovering, selling pressure is easing, and the coming weekly close will show whether this is the beginning of accumulation or just another short-lived rebound.

⚠️ Not financial advice.

#Ethereum #ETH #Bitcoin #Crypto

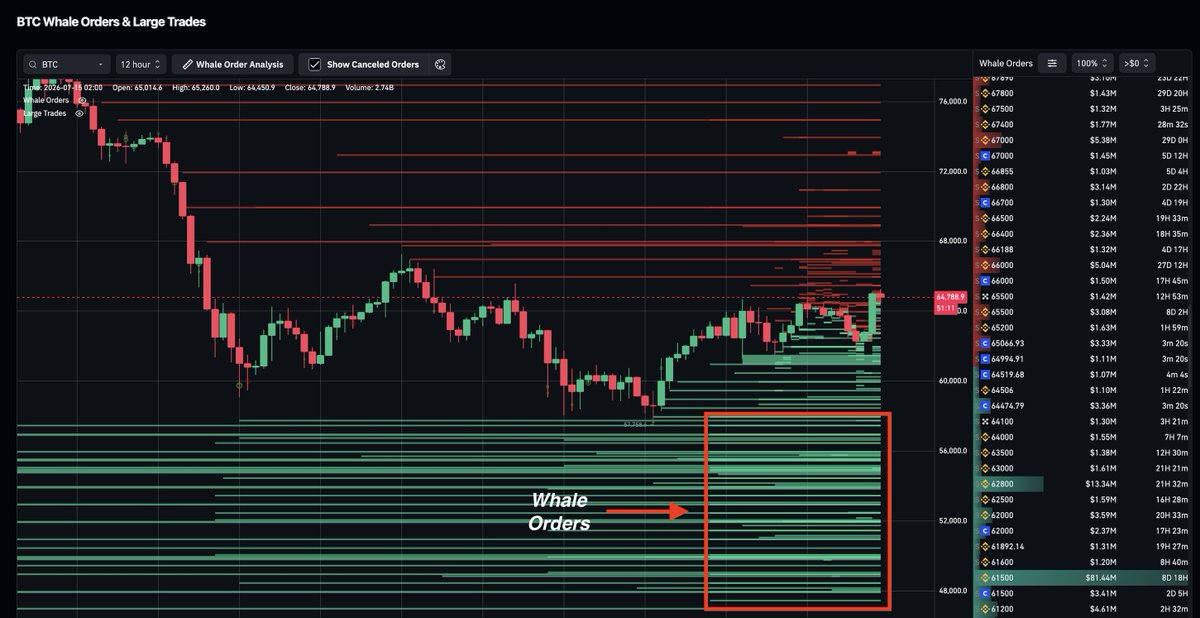

Here's why I think Bitcoin drops lower first.

Whales are stacking massive $BTC bids below the current price.

There's a HUGE wall of buy orders stretching from around $57K down into the high-$40Ks.

One single bid alone is worth $81 million at $61,500.

Smart money appears to be positioning for more downside before the next major move higher.

ビットコイン相場分析

まず、今日入ってきた特大のニュース。

ついに日本の国会で、暗号資産の税率を一律20.315%の申告分離課税へと移行する法案が成立。

これまで最大55%の雑所得として扱われていた暗号資産が、株式やFXと同等の正式な金融商品として日本国に認められた歴史的な瞬間。

3年間の損失繰越控除も導入され、

日本国内の投資環境は一気に激変する。

先日、ホワイトハウスでトランプ氏が放った「大の仮想通貨人間でありファンだ」という発言の追い風もあり、国内外から強力な買い材料が連発している状況。

だが、この裏で、今もう一つの特大ニュースが世界を揺るがしている。

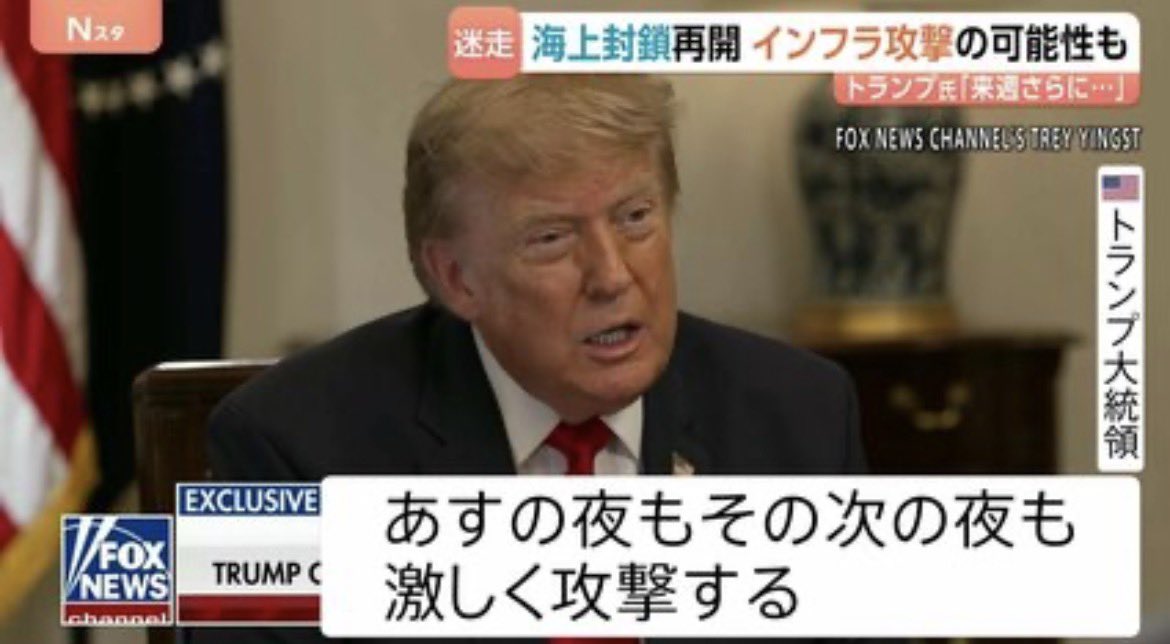

それが、トランプ氏による「ホルムズ海峡の海上封鎖再開」と「通過貨物への20%課税」という宣言。

これに対抗してイランも海峡の再封鎖を宣言し、中東の地政学リスクが一気に沸騰。

原油価格が再び跳ね上がり、

世界的なインフレ再燃の懸念がリスク資産であるビットコインの重しになり始めている。

【中長期結論】

歴史的な税制可決という「光」と、中東危機の再燃という「影」が同時に押し寄せ、市場は引き裂かれている状態。

目先のニュースによる上昇は、

大口の利益確定の出口として利用される可能性が極めて高い。

どれだけ材料が錯綜しても、

トレードで勝つために必要なのは目の前のチャートの事実のみ。

【BTC 短期目線】

ロング: 64,480 or 65,050

ショート: 64,340

リアルタイムでの進捗、TP,SL知りたい人は「イイネ&RT」しておいてね。

Most people are missing the ETH angle behind Robinhood Chain.

At first glance, it may seem like Robinhood launching its own chain has little to do with $ETH. The activity happens on Layer 2, fees are low, and users may never think about Ethereum mainnet.

But the deeper point is security.

Ethereum L2s do not exist in isolation. They rely on Ethereum mainnet for settlement, data availability, and security. If Ethereum’s security were compromised, assets and applications on its L2 ecosystem could also be affected.

According to the Ethereum Foundation’s report, around $76B worth of ETH is staked to secure Ethereum. The report also estimates that it would take about $50.7B worth of ETH to finalize a fraudulent transaction.

That is why institutional adoption on Ethereum matters for ETH.

Robinhood may be only one of the first major traditional finance platforms to build on Ethereum’s L2 ecosystem. If more banks, brokers, fintechs, and asset managers follow, the amount of value relying on Ethereum security could grow from hundreds of billions to trillions of dollars.

At that point, ETH is no longer just a gas token.

It becomes the economic collateral securing a global settlement layer.

That is the bullish case: as more real-world financial assets move onto Ethereum and its L2s, the market may be forced to reprice ETH based on the value it secures.

明显感觉现在 $ETH 讲故事的能力都不如 $NEAR了:

1) @NEARProtocol 是一条典型热衷讲故事的layer-1链,最早炒潜在的以太坊杀手,到后来的夜影分片,再到后来围绕创始人 @ilblackdragon Transformer架构共建者的AI叙事炒作,Near也许在币价暴力拉盘上缺席了,但讲故事这块始终杠杠的;

2)现在的NEAR吧Illia的Transformer背景、Intent-centric、保密执行,量子就绪,用户自由AI等打包进一个Agent-Economy的大叙事里,在整个AI主流叙事下,很难短期被证伪,又某种程度凸显了“团队在做事”的活力;

以上。

有朋友说,ETH不是不讲故事,只是不屑于讲,也是一个立场角度。的确,在当下只会讲故事并不是一个好的Buff。

见仁见智,但在Crypto技术创新枯竭,主流资金处于观望的态度下,个人认为,有些故事还是得继续讲的,毕竟包括SpacX、Anthropic、美光等在内的美股巨头也都少不了讲故事。

嗯,大ETH,故事讲起来噻! @VitalikButerin

HL 的优先费应该是最被低估的 $HYPE 赋能来源,也是近期崛起最迅速的赋能来源。

功能上线仅3个月时间,优先费的总收入占比稳步上升,目前占HL 协议总收入的比重达到7.3%。

值得关注的是, @HyperliquidX 近期更新了官方文档,将优先费的机制从只限“吃单者”拓展到“做市商”,做市商也能竞价(变相燃烧HYPE)“maker 队列优先权”。

可以预见的是,针对做市商的ALO priority 主网上线后,优先费占比将迅速突破2位数。

How will SK Hynix’s ADR listing impact the tokenized equities landscape?

The hottest story in the US stock market right now is SK Hynix’s US ADR listing.

It is set to raise around $26.5B, and demand has been insane, with the book reportedly more than 7x oversubscribed.

But here’s the interesting part.

Recently, Korean equities have been getting a lot more attention, and many platforms have wanted to tokenize Korean stocks.

The problem is that Korean stocks can only be traded in the Korean market, which makes it extremely difficult for platforms to source the underlying shares and tokenize them on a 1:1 collateralized basis.

So until now, the workaround has been platforms like @tradexyz and @QFEX launching perpetual futures markets that track SK Hynix, with investors trading exposure there instead.

Now that SK Hynix is listing in the US via ADR, the setup changes.

Platforms can now source SK Hynix ADR shares through US brokers like @AlpacaHQ.

That means issuer-sponsored tokenization platforms like @Securitize, as well as third party-sponsored tokenization platforms like @RobinhoodApp, @OndoFinance, and @xStocksFi, could potentially acquire SK Hynix ADR shares and start tokenizing them on a 1:1 collateralized basis.

In other words, we could soon see tokenized SK Hynix equities like SKHYx, SKHYon, and similar products.

Korean financial regulators have been watching closely as Korean stocks start trading on offshore perpetual futures platforms.

But if tokenized equities backed by SK Hynix ADRs are launched, and those tokens can freely trade onchain and be used across DeFi, this could become a real headache for regulators.

Especially because in the case of third party-sponsored tokenization, there is not much they can do to stop it.

So the big question is:

- Will tokenized equities based on Korean stocks start coming to market now?

- And how will Korean regulators respond?

Worth watching closely.

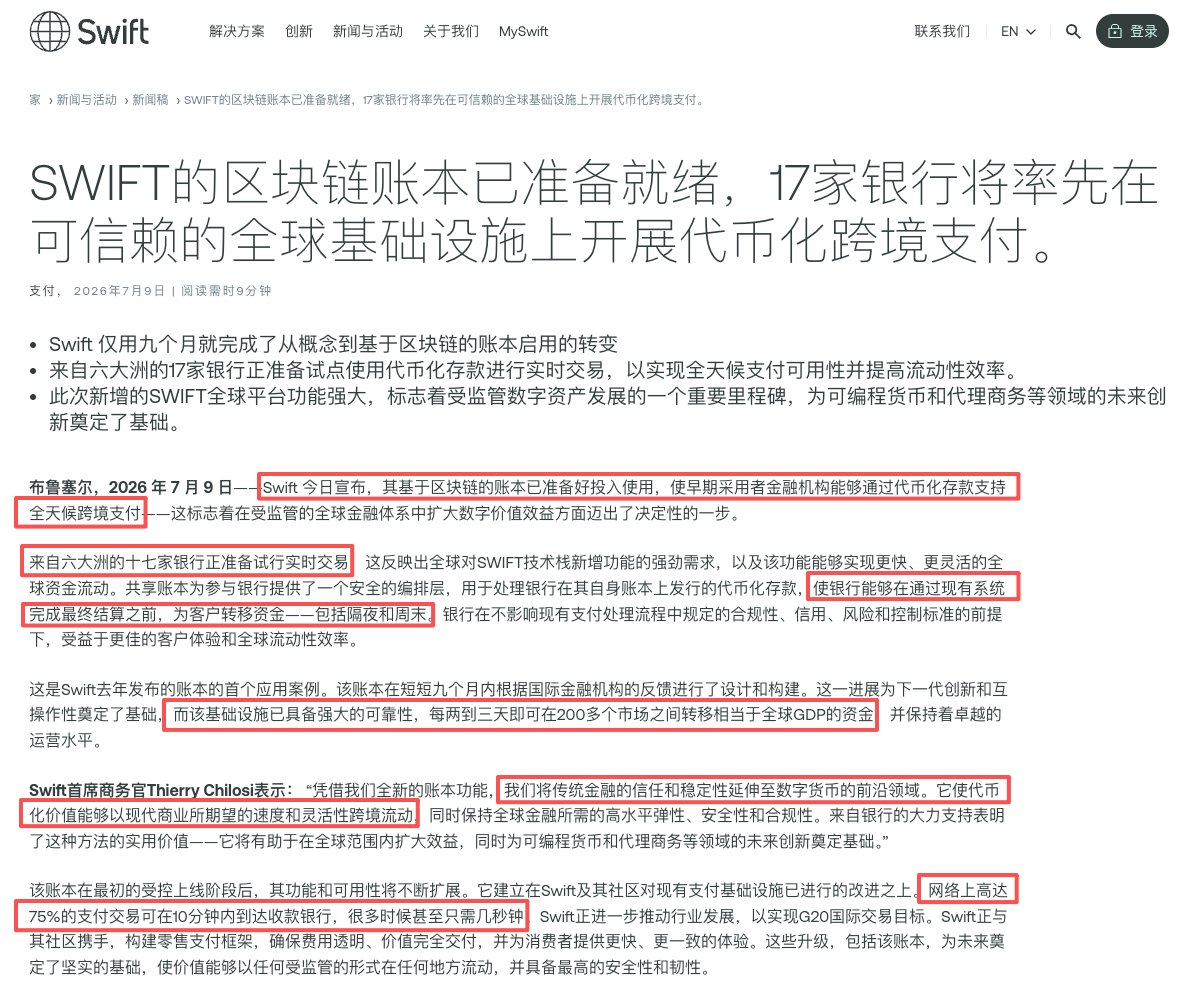

全球最大的金融网络Swift在今天宣布开发的区块链已经正式上线,首批接入了17家银行开展24/7代币化存款的跨境支付,从而实现秒到账,不再需要等待各个不同国家银行的营业时间,并且号称每3天就可以在200多个国家转移全球GDP的资金,这是传统金融体系对区块链和代币化迈出最大的一步,但也只能说迈出了半步,毕竟依然用的是联盟链,不过这也情有可原,但是转移的资金也依然不是USDT、USDC等任何一个稳定币,而是银行自己的代币化存款,只在Swift银行体系内部流转,所以这是以Swift牵头全球银行联合发起的一场防御反击战。

毕竟稳定币实时转账的优势摆在这里,如果Swift和银行再不行动,则很多企业会选择把银行存款换成稳定币,银行会失去存款,而Swift也会失去结算地位,所以Swift就拉着这些银行把自己的存款代币化,至少保证在原有体系里的资金不会流出去。

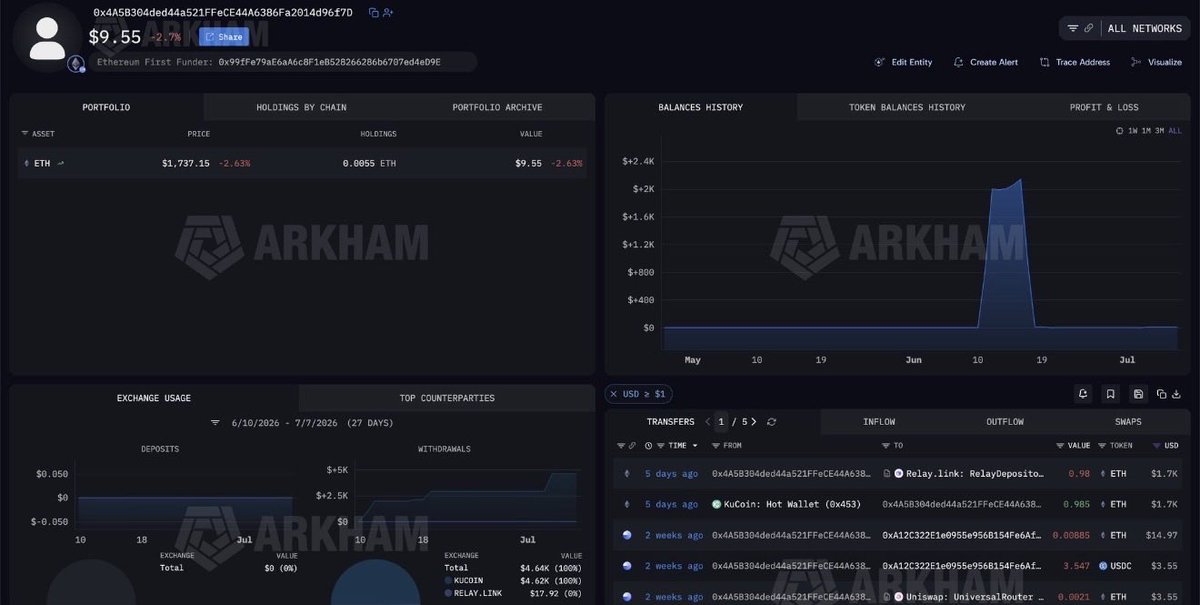

以太坊生态的 L2 链 Robinhood推出不过约一周时间,看起来正处于流量与流动性快速聚集阶段。

链上出现了一个有意思的案例:

一位交易者(地址 0x4A5B304ded44a521FFeCE44A6386Fa2014d96f7D)在 CASHCAT 市值仅约 7400 美元 时,以约 316 美元 买入该 ERC-20 MEME 代币。

目前其市值已超过 1 亿美元,实现超过 1.5 万倍的回报,浮盈超过 200 万美元。

该代币此前长期处于低位横盘,主要爆发集中在过去 24-48小时内,属于典型的 memecoin玩法:垂直拉升形态。

这玩家看起来像是一位顶级MEME 选手,

对叙事、时机和仓位管理都很在行,不仅单纯运气。

CASHCAT的叙事有历史渊源,它来源于 Robinhood 公司早期的内部历史。在创立初期曾考虑或内部使用 “Cash Cat” 作为昵称/备选名称,联合创始人 Vladimir Tenev 曾在公开场合提及这一细节。

刚好最近Robinhood Chain 主网上线,这一 lore 与官方事件形成了强绑定,迅速成为链上最具辨识度的原生叙事。

有意思的是,Robinhood 高管此前对 memecoin 整体持相对谨慎态度(Tenev 在主网前后公开表示更看好 RWA)。但在 CASHCAT 快速聚集大量交易量和用户注意力后,高管转为公开认可链“也适合 meme 生态”。😂

毕竟,新链需要流动性、用户和开发者注意力,而高热度 meme 能在短期内有效制造这些流量。

新链主网窗口期确实是稀缺机会。上线初期注意力最为集中,一旦某个 token 率先形成正反馈(交易量、持有人数、社交讨论),就可能快速强化链上流量。

若未能抓住,后续再吸引同等注意力的难度会大幅上升。

这也是为什么早期低市值入场能实现极端乘数,7400 美元市值本质上接近“空气”,流动性极薄,任何像样买盘(尤其是嗅觉敏锐的聪明钱)都容易引发连锁反应和 FOMO。

Uniswap V3 在 Robinhood Chain 的原生部署进一步降低了交易门槛。

一旦启动,KOL 跟进、社区 meme 传播与链上交易量形成飞轮效应。

从链上行为看,这位玩家很可能在链部署前或极早期就进行了研究(监控新合约、挖掘 lore 等),并采用极小资金测试的方式验证机会。

这正是顶级 degen 的标准打法:用可接受归零的仓位博取不对称回报,同时通过早期研究建立信息优势。因为在当时,谁也无法 100% 确定最终能否起飞。

总结来说,这是一次叙事、时机与执行的强力结合。

找到强叙事、极早入场、小仓位验证、拿得住主升浪,这些能力在 MEME 赛道要求极高。

绝大多数类似尝试最终都会归零或大幅回撤,超过万倍的回报案例可遇不可求。

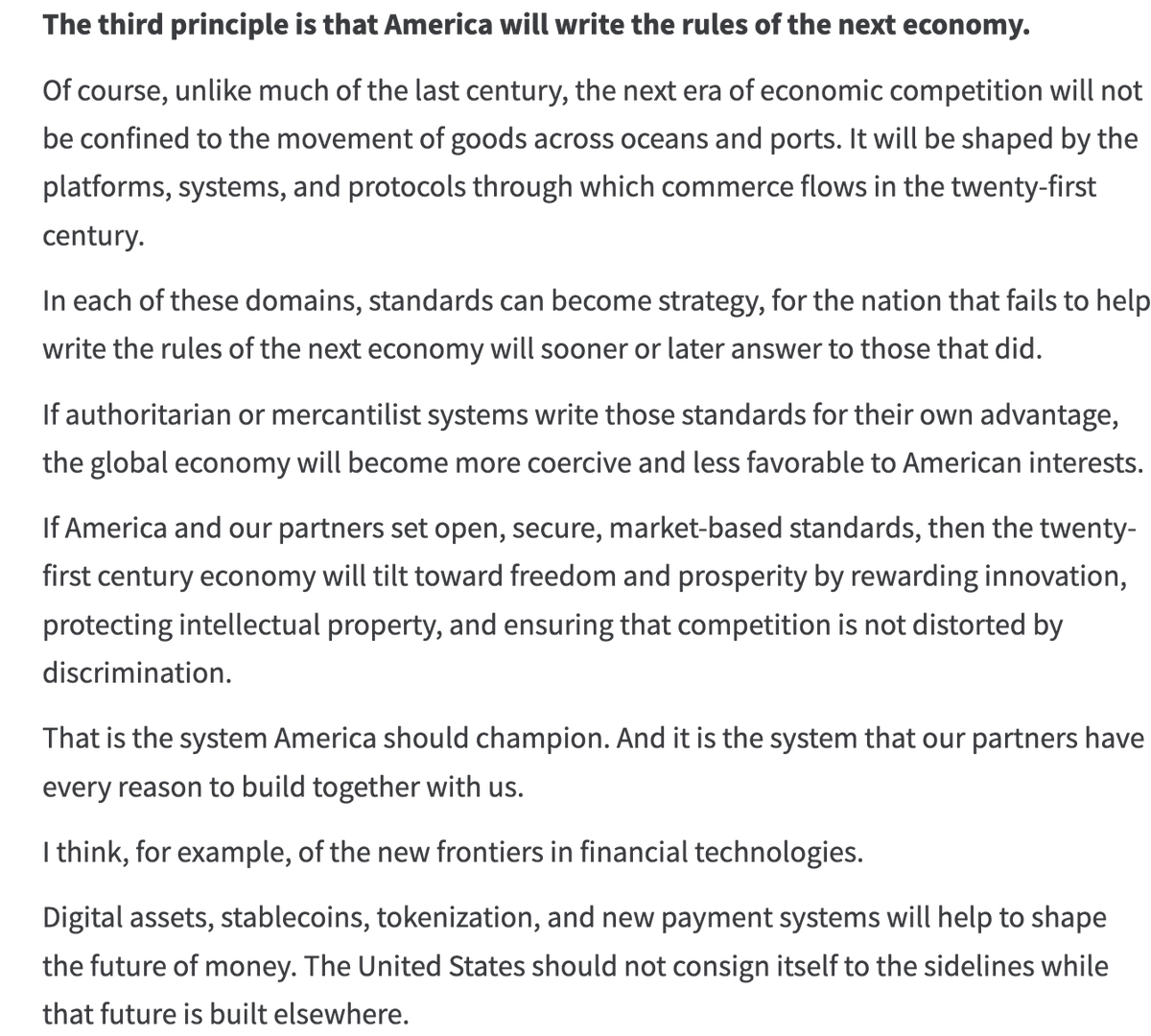

Spent my morning reading this recent speech from @SecScottBessent. It lays out a new and defining vision for America's role in the economy for the next 100 years. @elerianm calls it a "remarkably important speech."

Bessent organizes his vision around five principles. Principle 3 is, "America will write the rules of the next economy." He gives one example of what this means:

"Digital assets, stablecoins, tokenization, and new payment systems will help to shape the future of money. The United States should not consign itself to the sidelines while that future is built elsewhere."

If you've wondered how committed Washington is to making crypto succeed in the US, that tells you something.

日历

7 月 20 日暂无重要事件