arndxt

Twitter

观点

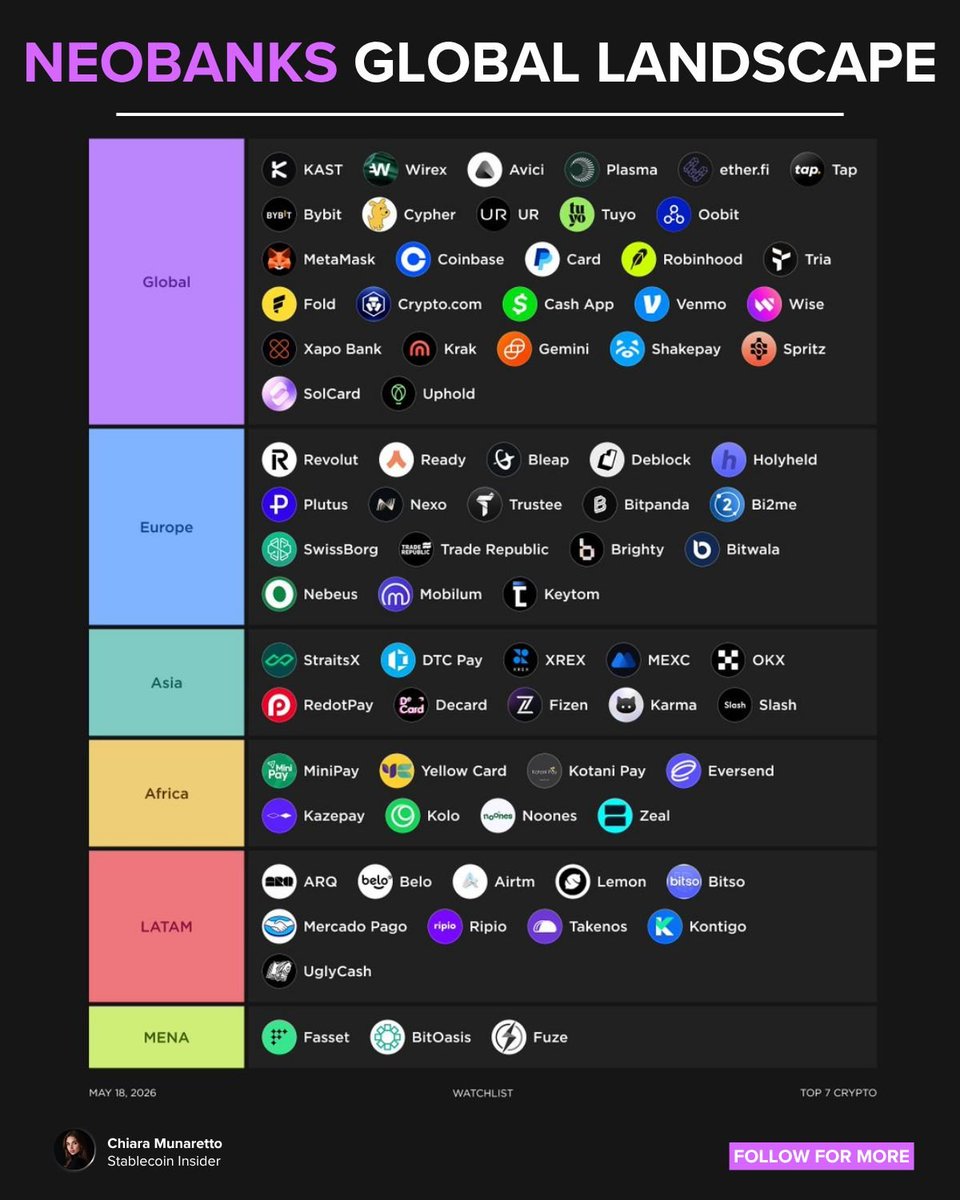

neobanks are being squeezed from two directions.

from the top, fintechs are pursuing bank charters to capture the economics they used to rent from sponsor banks: deposits, net interest income, payment access, and regulatory legitimacy.

from the bottom, stablecoins and public blockchains are rebuilding parts of the financial stack as open, programmable rails.

the result is compression.

the fat app thesis worked here, with the old neobank model being mostly a distribution layer:

- app + brand + customer relationship

- no balance sheet

- no direct rail access

- no deposit economics

the winning playbook is to own the economics. banking value does not accrue primarily to ux. it accrues to monetizable control points across store > move > grow > borrow money, such as:

- deposits

- credit

- settlement

- compliance

- liquidity

- customer trust

a neobank without these is just a frontend with rented economics.

this is why charters matter. a charter turns a neobank from a customer-acquisition machine into a balance-sheet business.

but charters are only half the story.

stablecoins attack the same stack from below by making settlement global, programmable, and cheaper. they weaken the monopoly of gated rails like ach, swift, and correspondent banking.

so the winning model is hybrid financial infrastructure: a mix of tradfi + crypto.

- regulated balance sheet where trust is required

- blockchain rails where speed and programmability matter

- defi protocols where financial products can be composed

- consumer apps where the relationship is owned

the future neobank is therefore not just a bank app.

most fintechs monetize only one layer. the trillion-dollar neobank captures all four.

this creates clear winners and losers.

winners:

- chartered fintechs

- crypto exchanges with distribution

- wallets that become financial apps

- defi protocols with real integrations

- stablecoin rails embedded into consumer finance

losers:

- middleware-dependent neobanks

- remittance firms relying on fx spreads

- wallets with no monetization

- banks with legacy ux

- defi protocols with no distribution

financial infrastructure is becoming more modular at the backend, but more consolidated at the frontend.

users will not care whether yield comes from a bank deposit, tokenized t-bills, @aave, @Morpho, or a stablecoin vault.

they will care about one thing if the app can be trusted to help them store, move, earn, borrow, and spend money better than their bank.

that is the endgame.

the bank account becomes a wallet.

the wallet becomes a bank.

the winner owns the interface between regulated finance and permissionless rails.

everything else is rented infrastructure.

i am a huge proponent of privacy $ZEC and recently:

- shared the desci narrative

- caught onto $ONDO with a 2x

- money/credit markets like $AAVE $AERO $MORPHO

- $HYPE has been the strongest thesis along with several ai companies given their similar verticalization approach

there are alpha to some early projects which you should also explore

👇

1) @SeismicSys

privacy-first blockchain with normal ethereum developer experience. developers can build private apps without learning a totally new language or stack. most privacy chains require special tooling, new languages, or complex cryptography. Seismic tries to make privacy feel like normal Solidity/EVM development.

- $17M total raised (latest $10M led by @a16z crypto + @polychain + others in late 2025).

- testnet live since early 2025 (faucet + devnet activities ongoing, community is farming for potential airdrop).

- partners like @brookwellapp already routing stablecoin flows.

- narrative fit is perfect (privacy + real fintech adoption).

- this has the strongest VC signal in the list.

2) @tmrwfinance

creator lending against future AdSense revenue. youtubers and digital creators can borrow based on expected future income. Karat is more like banking for creators. Spotter buys catalog rights. Tomorrow uses a lending model, so creators can get capital without selling ownership of their content.

- very early/stealthier than the rest.

- part of @base ecosystem cohorts.

- fits creator economy + RWA lending narrative but less public traction/funding visible yet.

- underdog play vs bigger tokenized credit names.

3) @lightconexyz

trade the impact of events, not just whether events happen. it answers: “what happens to ETH/BTC/SOL if this event occurs?” prediction markets trade probability. options trade price movement but not clean event-specific outcomes. lightcone creates state-based assets, so users can hedge very specific scenarios directly.

- product site live.

- still pre-token/early.

- volves prediction market narrative into something more useful for hedging real outcomes.

- low competition in this exact flavor.

4) @techdollarhq

borrow against private tech shares without selling them. Employees or early investors in companies like AI labs or frontier tech firms can access liquidity while keeping upside. we recently saw @OpenAI employees sold $6.6b of equity and instead of selling, they can get a loan. Forge and EquityBee mostly focus on secondary sales or option financing. TechDollar focuses on lending against private equity, closer to margin lending for private startup shares.

- product page live with waitlist + clear borrower thesis (frontier tech conviction without forced exits).

- bridges TradFi private equity illiquidity with crypto-style credit.

- no big funding announced yet but clean positioning in the private shares as collateral narrative.

5) @agra_gg

secondary market for tokenized private credit. it lets holders exit before maturity instead of being stuck until redemption. most tokenized credit platforms only solve issuance. Agra solves liquidity. Its yield-based orderbook also fits bonds better than normal AMMs or price-based trading.

- beta live on Ethereum right now with real markets like Anemoy/Apollo credit fund and others.

- tokenized private credit is one of the hottest RWA sub-narratives ($14B+ already in the space).

- first-mover liquidity layer here is real product alpha.

6) @OrnnExchange

commoditizes GPU access. it treats compute like oil or electricity: a scarce resource that should be priced, traded, and accessed efficiently. most GPU projects are just marketplaces. Ornn’s bigger idea is that GPU compute becomes a financialized commodity layer for the AI economy.

- $5.7M seed (oct 2025).

- index already on Bloomberg Terminal.

- live spot pricing + derivatives coming.

- perfect AI infra narrative, compute as the new oil.

- regulated U.S. venue angle is big for institutions.

7) @numoforex

fx infrastructure for frontier markets that gives currency hedging tools to markets where normal fx products are missing or too expensive. most fx platforms serve large institutions or developed markets. Numo targets the places where fx risk is most painful but least served.

- product live with actual markets and volume.

- zero-fee on/off-ramps.

- targets painful real-world FX risk in underserved markets.

- one of the few actually shipping frontier FX infra.

8) @meanwhile

bitcoin-native life insurance. it connects long-term $BTC holding with long-term financial planning. most bitcoin products are trading, lending, or custody. Meanwhile treats btc as a long-duration savings asset, closer to insurance and retirement planning.

- massive $82M raise (oct 2025).

- first and only licensed BTC-native insurance carrier.

- huge signal for BTC as serious savings vehicle beyond trading/lending.

- institutional partner push incoming.

9) @merit_systems

from builder reputation to AI-agent commerce. it started by tracking and rewarding open-source contribution, then moved toward payments/commerce for agents. most reputation systems are static badges. their newer direction is more dynamic: enabling AI agents to transact, earn, and interact economically.

- shift to agent economy is perfectly timed with AI agent hype.

- live tools (AgentCash, Poncho, directories).

- enables permissionless agent-to-agent commerce.

- narrative tailwind is massive.

10) @StreetFDN

tokenizing startup equity. it builds standards and infrastructure to make private startup shares easier to issue, manage, and transfer. equity tokenization usually focuses on public stocks, funds, or bonds. Street targets startup equity, which is illiquid, paperwork-heavy, and structurally hard to access.

- claims 150+ startups tokenized.

- solves paperwork + access issues in VC equity.

- fits the broader equity tokenization wave (SPV wrappers are the current compliant path).

- early mover on actual startup (not public stock) side.